One of my lectures at Mises University each summer concerns environmental issues. I make changes every year, but I always mention Murray Rothbard’s essay “Law, Property Rights, and Air Pollution.” In it, Rothbard lays out a libertarian method for handling what mainstream economists usually call externalities—the side effects of production or consumption activity on bystanders. The contrast between Rothbard’s welfare economics and the mainstream is plainly visible. Whereas many mainstream economists try to measure costs and benefits of pollution in order to come up with the most efficient level of pollution, or the appropriate tax to impose on the polluter (a la A.C. Pigou), Rothbard strictly eschews any such effort to measure the immeasurable.

Emissions Taxes and Tradable Permits

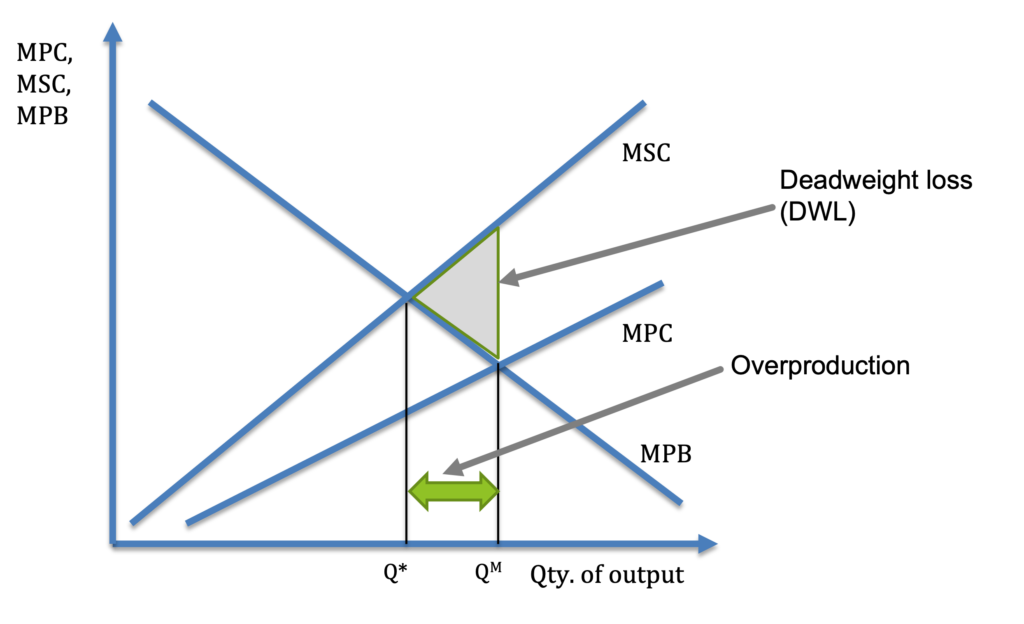

The typical presentation of negative externalities involves something like the diagram below, where the costs on bystanders are added to the marginal private costs (MPC) faced by the polluting firm, to come up with a marginal social cost (MSC) that, along with the marginal private benefit (MPB) to the firm from producing its output reveals the ideal level of output. In the presence of these negative externalities, and absent positive externalities that would offset these, the market level of production QM is too high, compared to the welfare-maximizing level of production Q*.

As court-made law to settle conflicts over nuisances like pollution has been increasingly regarded as inadequate to deal with externalities, government interventions have typically taken three forms: 1) command-and-control regulation, 2) emissions taxes, or 3) cap-and-trade systems.

Command-and-control regulation has significant problems which I will not spend much time on here. It is unpopular with many economists because of its tendency to mandate emissions reductions in ways that are inflexible and therefore likely to be more costly. Public choice economists have pointed out that command-and-control is also vulnerable to political “rent-seeking” since particular technologies can be mandated to confer benefits on those who make the technology or who are competing with firms that cannot easily afford the technology.

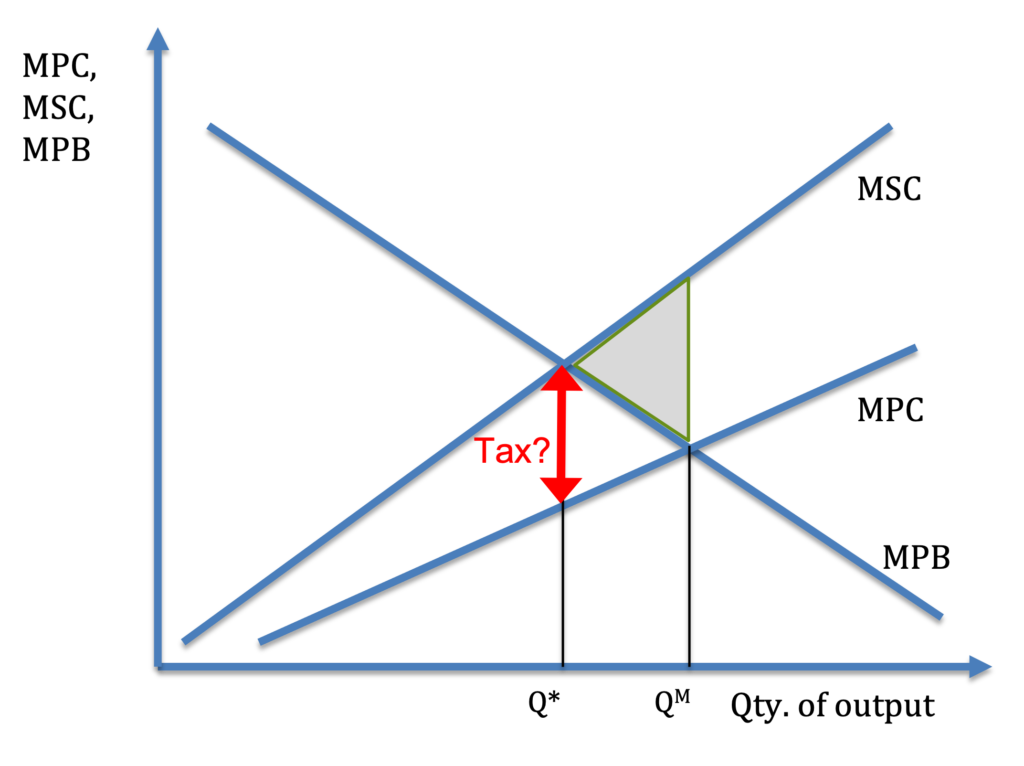

Emissions taxes are supposed to bring the marginal private cost in line with the marginal social cost by forcing the polluter to account for the external cost via a tax bill:

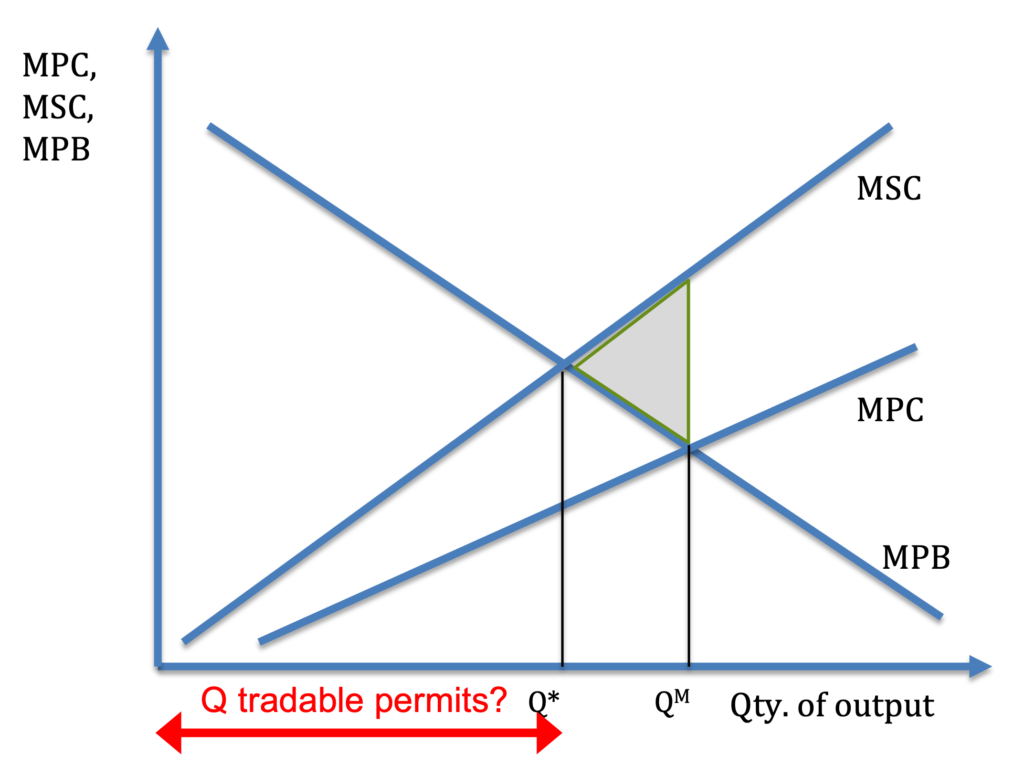

A tradable permit is intended to accomplish the same result by identifying the optimum level of pollution and distributing pollution permits to allow that quantity of emissions. The method of initially distributing these permits is a matter of some debate, but economists tend to appreciate the market features of these systems.

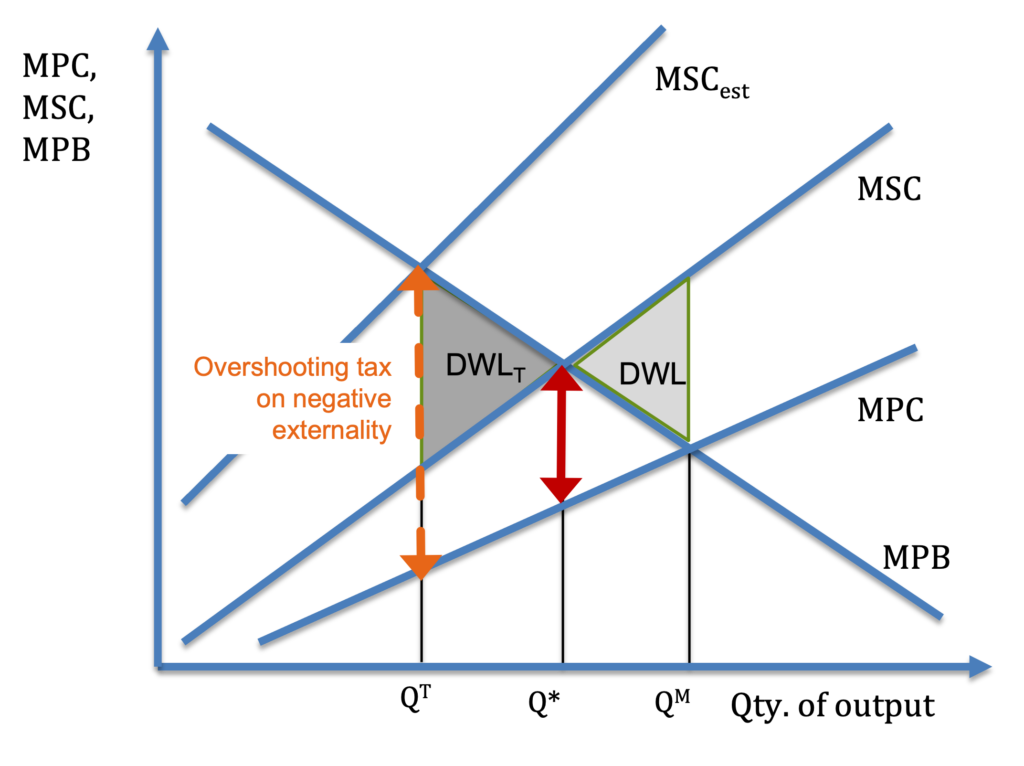

Returning to emissions taxes, we must recognize the distinct possibility of overshoot–a tax that is based on an erroneously high estimate of marginal social cost. In such a case, from any reduction in deadweight losses obtained from the emissions tax, we would have to subtract any added deadweight loss (DWLT) to the left of the optimum point in the diagram below.

If the tax is high enough, it could result in deadweight losses that are higher than the deadweight losses resulting from the untaxed negative externality. Because, again, governments have no way to discover the MSC, there is no way to determine whether the emissions tax has improved the situation from the initial point with no government intervention—and it is quite possible that the situation is worse rather than better. Similarly, a tradable permit system that selects a quantity of output that is too low could have an equivalent undesirable result.

James Buchanan explains the difficulty, in Cost and Choice:

Consider first, the determination of the amount of the corrective tax that is to be imposed. This amount should equal the external costs that others than the decision maker suffer as a consequence of the decision. These costs are experienced by persons who may evaluate their own resultant utility losses…. In order to estimate the size of the corrective tax, however, some objective measurement must be placed on these external costs. But the analyst has no benchmark from which plausible estimates can be made. Since the persons who bear these ‘costs’–those who are externally affected–do not participate in the choice that generates the ‘costs’ there is simply no means of determining, even indirectly, the value that they place on the utility loss that might be avoided.

J. Buchanan (Cost and Choice, 72)

As Art Carden succinctly put it, “The information needed to know whether a particular regulation ‘works’ quite literally does not exist, and the key difference between firms and governments is that firms… have market tests for their decisions. Governments do not.” (Carden 2014, 221)

Economists have long recognized this problem, but have been reluctant to face its implications. William Baumol, writing in the AER in 1972, admitted these difficulties in a defense of Pigovian taxes:

Despite the validity in principle of the tax-subsidy approach of the Pigovian tradition, in practice it suffers from serious difficulties. For we do not know how to estimate the magnitude of the social costs, the data needed to implement the Pigovian tax-subsidy proposals. For example, a very substantial proportion of the cost of the pollution is psychic; and even if we knew how to evaluate the psychic cost of some one individual we seem to have little hope of dealing with effects so widely diffused through the population.

W.J. Baumol (1972, 316)

Baumol essentially dismissed these problems and proposed acting “on the basis of a set of minimum standards of acceptability,” finding “some maximal level of this pollutant that is considered satisfactory….” (318) This of course sweeps the information problem (how much is “acceptable” or “satisfactory”?) under the rug, which he admitted (320).

Added to the information problem is the incentive problem governments face. When confronted with various interest groups that would like to use the emissions tax or permitting or regulatory apparatus to promote their own ends—which a survey of “bootleggers and Baptists” alliances indicates is not uncommon—policymakers may find that seeking Q* as opposed to a suboptimal point like QT is politically untenable. The political “rent-seeking” that goes on among competing groups wishing to push the tax higher or lower is itself costly.

Rothbard vs. Coase

Rothbard also avoids the problem created by Nobel laureate Ronald Coase, who wrote in his famous 1960 essay in the Journal of Law and Economics that if transaction costs were zero, all a court had to do is define property rights over a disputed resource (like air or water) and the two disputants would arrive at an efficient solution through bargaining after the case was decided. This approach is attractive to those who are inclined to protect property rights and let markets sort out solutions through private bargaining.

Transaction costs, of course, aren’t zero, as Coase well knew, and therefore courts would end up making decisions about efficiency—which of course requires interpersonal utility comparisons that they are unable to carry out.

There are many Coaseans who would be regarded as market-worshiping cultists by those who favor regulation to handle environmental problems, but from Rothbard’s point of view, Coase requires the sacrifice of property rights even as private bargaining takes place.

As Rothbard points out the insurmountable subjective value problems that afflict Coasean analysis, he moves toward ethics as the appropriate foundation for resolving these externality problems. Ethics, he points out, are embedded in Coase’s analysis:

Another serious problem with the Coase-Demsetz approach is that pretending to be value-free, they in reality import the ethical norm of “efficiency,” and assert that property rights should be assigned on the basis of such efficiency. But even if the concept of social efficiency were meaningful, they don’t answer the questions of why efficiency should be the overriding consideration in establishing legal principles or why externalities should be internalized above all other considerations. We are now out of Wertfreiheit and back to unexamined ethical questions.

M.N. Rothbard (1982, 125, 126)

Two valuable contributions to environmental economics from an Austrian perspective are Roy Cordato’s 2004 “Toward an Austrian Theory of Environmental Economics” in the Quarterly Journal of Austrian Economics, and his 2007 book Efficiency and Externalities in an Open-Ended Universe. An interesting exchange on Austrian economic thinking about pollution, Coase, etc. has occurred over several decades in the Journal of Libertarian Studies, the Review of Austrian Economics, the Quarterly Journal of Austrian Economics, and elsewhere, with Walter Block (1977, 1995, 2000, and 2010, and 2014), (Coasean) Harold Demsetz (1979, 1997), Michael Brooks, Art Carden, and Ed Dolan (2014 and 2015) contributing.